| 8 mins read

SUMMARY

- Over the decades, government support for home ownership has shifted from making tax concessions to households and providing building subsides for local authorities, to a centrally driven housing programme focussed around a myriad of part-rent part-own and equity sharing schemes alongside the Right to Buy.

- Labour faces difficult decisions regarding housing priorities, not least given budget constraints.

- While its focus will understandably be on providing more social rented homes, there is still a need to assist meeting aspirations around home ownership.

Over time we have seen multiple initiatives aimed at boosting levels of home ownership in the UK. What more might be done, if anything, to build a more effective first rung on ‘the ladder’?

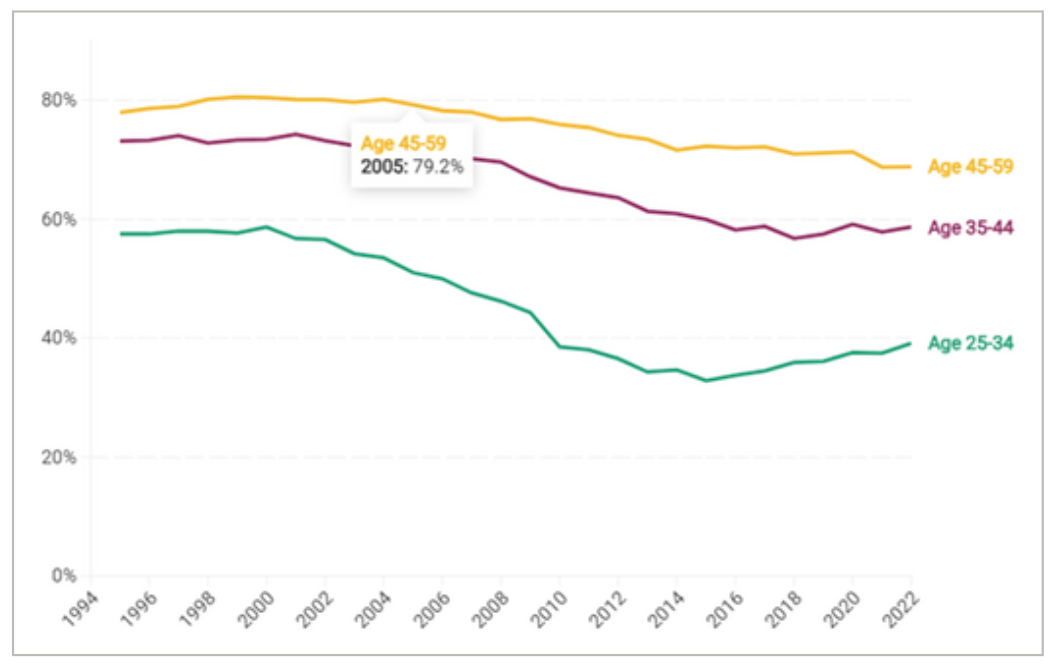

As Figure 2 highlights, since 1995 home ownership levels amongst younger households in the UK have fallen. While a recovery has been underway in more recent years, they are still significantly reduced and not least for 25–34-year-olds.

Figure 2: Homeownership rates of working-age adults, by age group, 1995–2022.

The rate of home ownership has fallen in lower socioeconomic groups. Between 2 and 3 million households who we might have expected to become owners since 2006 have failed to do so.

Labour's rock and a hard place

Labour has arrived with a determination to tackle the ongoing housing crisis. To date, the policy focus has been firmly on supply-side solutions, for example, new towns and planning reform. The government's target for new housing supply in England is 300,000 homes a year and 1.5 million homes in the first parliament.

Where it has ventured towards tenures, the focus has been on upping the provision of social housing for rent, an utterly legitimate goal, but one that leaves open other unresolved issues. The government has also pledged to reduce inequality, boost opportunity and grow home ownership. In part, these objectives are intertwined. There is clearly huge dissatisfaction amongst younger voters as to their diminished prospects of being homeowners, and boosting social renting won't solve that. In reality, social renting and home ownership are not alternatives, but are complementary.

As matters currently stand, the government has shared ownership as its primary programme for tackling both demand and supply for affordable home ownership (there is also the lifetime ISA scheme to assist saving for a deposit). In recent years shared ownership has attracted considerable negative publicity. Flats make up around 40 per cent of the stock of shared ownership homes (60 per cent are houses), but flats dominate in London (80 per cent flats, 20 per cent houses). This would not be obvious from the press coverage, nor would it be clear that many of the failings ascribed to shared ownership are in fact a consequence of both the failings of leasehold tenure itself, as well as the recent cladding scandal.

Without doubt, shared ownership needs further improvement, but buyers’ demand typically exceeds supply, and there is an appetite from private investors.

The current consultation on reforming the right to buy in England suggests the government will still want to see long-standing tenants being able to buy their homes, and for local councils to be able to replace what is sold. Looking back, right to buy policy has made the biggest increase to the level of home ownership in the UK—perhaps up to 10 per cent higher—but that flow has tapered off over time as the social rented sector itself has become more focussed on poorer households.

With the rent-to-buy and first homes schemes delivering very small numbers (and both potentially being scrapped) we are thus left with the question of what next?

Low-cost home ownership schemes in the UK are supplemental, and have never been funded to deliver more than a relatively small number of affordable homes on an annual basis.

The future of home ownership

What then for home ownership in general, and low-cost home ownership in particular in an era of ever higher house prices?

Estimates suggest that upwards of 2 million renters or adults living with parents are would-be owners. Clearly there is a geography to where cheaper, more affordable homes can be found. The profile of homeowners will vary area by area. That, of course, poses challenges for any intervention around low-cost schemes.

While the number of first-time buyers with a mortgage was just over 341,000 in 2024, the fifty-year average is closer to 390,000, with individual years much higher. It is clear there is still a case for programmed interventions. In making the mortgage guarantee scheme permanent, the UK has at long last adopted the mainstream solution in place in advance economies elsewhere. However, without further adjustment, it is still unlikely to secure wide take-up. Even if that is achieved, it is not a universal panacea, and other support will be needed.

Given its longevity and its strengths in terms of reach across the income spectrum, and notwithstanding the need for further improvement, shared ownership should be part of this mix—it has a well-established delivery system, is based on new homes, is low-cost in grant terms and produces capital receipts for re-investment. A reformed right to buy, perhaps preferably via a transferable discount, probably then completes the picture.

The question, then, is whether any more is needed. Regulatory controls in relation to the mortgage market are being eased, which has allowed lenders to reduce the severity of their stress testing and increase their borrowing limits for borrowers.

Going forward, the government and the Bank of England could evolve a stronger objective around securing a more stable housing market. There are also schemes that might be added to the mix, such as the open market shared equity scheme (currently operating in Scotland) which helps people buy homes in the mainstream market, and the help-to-stay scheme in Wales which provides equity loans to those in difficulty. In the round, with more systematic and effective husbandry of the market we might see home ownership levels edge closer to what was achieved before.

The reality of the housing system is that, in addition to making the market function as effectively as it might over the economic cycle, only a small number of schemes carefully targeted and adjusted in the light of market conditions are needed to support home ownership at a level which can be sustained through that cycle. Too often the focus has been on entry to this first rung and not on the journey ‘up the ladder’. Ultimately, a low-cost home ownership programme needs to be linked to a wider view of home ownership, and to a comprehensive and integrated policy on housing tenure.

Need help using Wiley? Click here for help using Wiley