| 14 mins read

SUMMARY

- Many commentators critiquing the British state cite fiscal devolution to English local authorities as a desirable reform.

- But fiscal devolution is of questionable benefit unless it is well designed and located in a narrative of the purpose of local government.

- Claims that fiscal devolution guarantees more money, better accountability, improved decision making and increased growth for local authorities are not clearly borne out by experience in other countries.

- However, there are stronger rationales: namely the financial stability of local authorities; and leading the development of parity of esteem between central and local governments.

It is hard to overstate the scale of the financial challenges that local government funding in England faces. Research has identified gaps between projected funding and projected spending needs of £9.3 billion by 2026–27.

Local authorities across the UK are unusually constrained in their ability to raise local taxes. They are highly dependent on property tax revenues but have little power over tax rates or tax bases. In this context of crisis, fiscal devolution—giving subnational governments (SNGs) more power to raise money locally—appears a holy grail. A narrative emerged in England in the early 2020s that fiscal devolution would improve governance, deriving from sharper accountability to local electorates; increase growth and productivity, leading to increases in local revenue; sharpen the imperative to spend a limited stock of locally raised money well; and provide more money in the system, from more sources. Accordingly, many publications in recent years have referenced devolving taxation powers.

However, many of the benefits of fiscal devolution that are held out in the recent spate of proposals are questionable. This is not to argue that fiscal devolution is undesirable. But experience in other OECD countries points to two stronger alternative rationales for fiscal devolution, and these have implications for the design of any new system in England.

Fiscal devolution: who says, and why?

The limited sources of revenue available to English local authorities have been periodically critiqued since at least the Layfield Report in 1976. English local authorities’ only major source of revenue is recurrent property taxes—council tax and business rates. Many proposals have appeared in the early 2020s to introduce fiscal devolution for English local authorities. Some suggest devolving specific taxes, or tax shares. The Centre for Progressive Policy proposed devolving 2 per cent of income tax receipts to local government (of which 40 per cent would be redistributed between authorities) together with 2 per cent of VAT and corporation tax receipts. UK Onward proposed devolving 1p of income tax to metro-mayors, together with greater control over the business rates multiplier. The London Finance Commission's 2017 report Devolution: A Capital Idea proposed full control for London government over council tax, business rates and stamp duty.

Financial accountability and performance

The ‘benefit model’ of local government finance holds that local authorities are inherently more efficient when spending locally raised revenue, and that this makes them more accountable to their electorate. This model sees the ideal form of local government as one in which local electorates pay in full for local services, principally through property taxes and user charges.

Its simplicity is appealing, and the basic formula shapes much debate in the UK as it aligns neatly with the ‘Westminster model’ of government.

Concepts of accountability in UK governance are tightly bound up with finance. This is a one-dimensional view. In practice, electoral accountability based on voters’ assessment of spending is invariably complemented by financial oversight of SNGs by central governments, or independent bodies, and by national standards for particular services. In practice, electorates often do not know which tier of government does what. SNGs can face blame for outcomes over which they have no power, and they may not have sufficient funds to deliver what their voters want.

Most local authorities in the OECD are funded by a range of sources—even in countries with far more extensive fiscal devolution than in England. Instead of using increased ‘accountability’ or ‘autonomy’ as rationales for fiscal devolution, devolving taxes should be considered in the context of the overall financial profile, functions and legal duties of the relevant SNGs.

Growth

There is a consensus in the UK policy world, at least at the rhetorical level, that fiscal devolution to local government would drive economic growth. The government's English Devolution White Paper stated that ‘devolution to capable local leaders at strategic scales has been linked to higher productivity, meaning more money in people's pockets’. A parallel argument is that SNGs can be stimulated towards policy interventions that drive economic growth if they collect more tax receipts.

Many scholars too have argued that devolution to local government of powers to raise taxes enhances local growth. Yet other scholars have noted the difficulty of measuring the causal effects of fiscal devolution. Rodríguez-Pose and Ezcurra found a negative correlation between fiscal devolution and economic growth between 1990 and 2005.

Elsewhere, scholars have argued that fiscal devolution alone does not correlate reliably with growth or productivity levels or changes: the quality of governance by an SNG is also critical. Scottish fiscal devolution has not obviously driven increased growth; nor has the Business Rates Retention Scheme, for English local authorities, had any significant effects on growth rates since 2013.

More money in the system?

At first glance, fiscal devolution could be expected to raise more funds for SNGs. Central policy and legislation—as well as public opinion—prevent significant extra revenues being sought from the two local taxes, council tax and business rates.

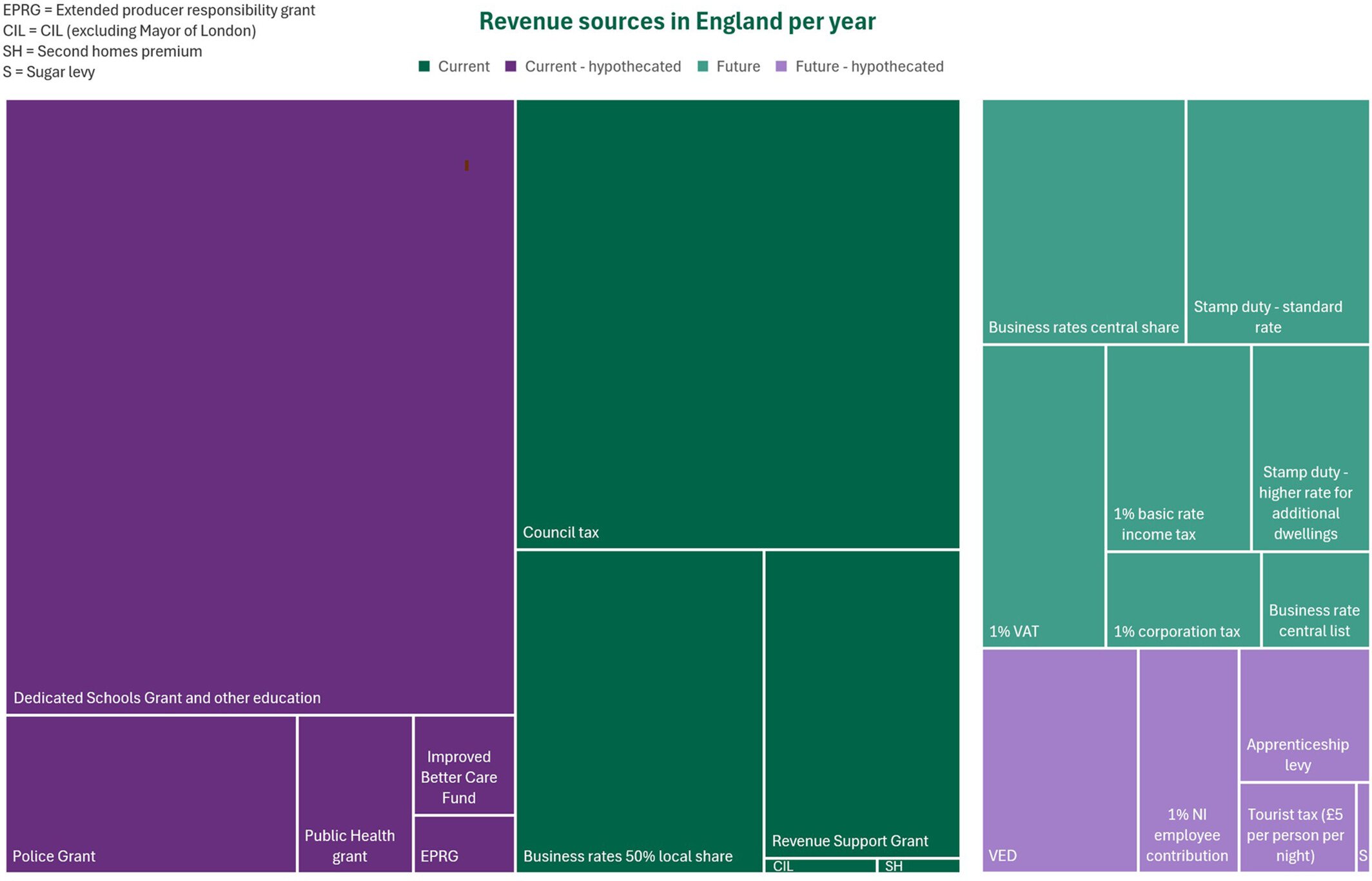

First, many of the sources of revenue that appear in think-tank publications produce sums of money that are marginal compared to total local government spending. This is illustrated by the treemap below.

Figure 1: Annual sources of revenue for local government in England and potential future sources of revenue, 2024–2025

The treemap highlights the gulf in scale between the revenue available from taxes proposed for devolution and English SNGs’ existing sources of revenue—in particular transfer grants and the Revenue Support Grant.

Many taxes proposed for devolution produce minuscule sums, which will have only a marginal effect on SNGs’ financial sustainability. For instance, the Institute for Fiscal Studies forecast that a visitor levy of £5 per person per night could raise £2.1 billion per year across the UK. This compares with total expenditure in the region of £100 billion per year across English SNGs.

Some smaller taxes are as much tools to tackle discrete policy challenges as means of increasing revenue. Many of them are ‘Pigouvian’ taxes, levied on negative externalities of economic activity. Internationally, legislative requirements often (though not always) require revenues from this type of tax to be spent on policies intended to remedy the identified externality. So, for example, funds from road pricing must be spent on transport. This makes budgetary flexibility more finite.

Core revenues also cannot be bolstered by sources such as borrowing, land value capture (LVC) and tax increment financing (TIF). These appear regularly in commentary, but they cannot be used to relieve day-to-day spending pressures, only for capital investment.

It is likely that any devolution of national tax revenues to English local government would lead to an equivalent sum in transfer grants being removed (substitution), so that local authorities did not receive a windfall. This was done in Scotland and Wales when fiscal devolution was introduced in the 2010s.

The figures in the treemap highlight that a system of fiscal devolution that was intended to increase SNG revenues substantially would, realistically, need to comprise shares of major national taxes such as income tax, corporation tax and VAT.

Many countries that are often cited as exemplars of fiscal devolution in fact provide much funding for their SNGs (both local and regional) through shared revenue systems. In these systems, local authorities don’t necessarily have control over the tax rates or bands. They may simply receive a share of the revenue raised in their area from the ‘devolved’ tax.

Shared taxes rarely replace transfer grants entirely. If the revenues from them fall below forecasts, or SNGs need additional funding, this is often negotiated with a higher tier. Central governments cannot ‘devolve and forget’.

Redistribution

Most taxes generate more revenue per capita in wealthy areas than in less buoyant areas. This effect is particularly stark in England owing to its high levels of geographical inequality.

Most advocates of fiscal devolution in England acknowledge the need for equalisation of funds alongside a system of fiscal devolution. Internationally, the norm is for substantial local revenue-raising powers to be accompanied by redistribution amongst SNGs, via a separate equalisation grant or horizontal redistribution or both.

In principle, receiving equalisation funding reduces a local authority's exposure to the benefits of efficiency and accountability arising from fiscal devolution. Thus, equalisation requirements alone undermine two of the rationales for fiscal devolution noted above.

Alternative rationales for fiscal devolution

If fiscal devolution does not necessarily provide economic growth, or additional funds or strengthened accountability for local governments, how would it improve local government funding and performance? I suggest that two stronger rationales for fiscal devolution exist. One is its potential to increase financial stability. SNGs with access to a basket of revenues are less exposed to capricious changes to grant systems driven by central policy initiatives. This increases their capacity to plan in the medium to long term.

A rationale for fiscal devolution can also be found in the field of intergovernmental relations. A system combining shared taxes, local taxes and transfer grants acknowledges that central and local (and regional) governments are engaged in a joint endeavour. This is an approach to government that has always been conspicuous by its absence in England and across the UK.

A fiscal devolution system’s effectiveness would depend on central-local relations institutions; the existence of a legislative framework; the existence of SNGs that had sufficient capacity and legitimacy to keep the confidence of other tiers of government and of the electorate; and the growth of a culture of collaborative governance.

What kind of ‘answer’ fiscal devolution provides depends critically on the question being asked. For instance, local authorities with statutory duties to provide major public services require sources of revenue that are substantial, non-volatile and redistributable, to provide equity and reliability. Thus, fiscal devolution for an SNG with broader service-provision responsibilities—and consequent high expenditure requirements—could align with the large and comparatively stable revenues available from income tax and VAT (and to a lesser extent corporation tax). The existence of national entitlements to services would provide a rationale for additional equalisation grant funding.

On the other hand, SNGs with growth-related missions, such as England's new mayoral authorities, might benefit from sources of revenue that are smaller overall but that have more scope for pro-cyclical variations in revenue. In the English context, this could point towards mayoral authorities that are focusing on transport, skills and public health gaining access to local revenue from a visitor levy, road pricing, an apprenticeship levy and a sugar (or other public health-related) levy. That revenue would reduce their dependence on grant funding and highlight, for public and stakeholder benefit, the range of their responsibilities.

It is understandable that policy makers and commentators have sought to build a case for fiscal devolution by focusing on concepts like ‘growth’ and ‘accountability’. These are much more politically appealing than the abstractions of governance, financial stability and parity of esteem. But proposals for fiscal devolution are not likely to find favour with governments if they begin with unrealistic aspirations. The purposes of fiscal devolution provide a starting point for concrete proposals: selecting sources of revenue to be devolved, estimating their financial impact and situating them in the broader functions and missions of SNGs.

Need help using Wiley? Click here for help using Wiley